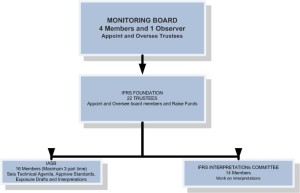

What Constitutes the IFRS Organization?

- MONITORING BOARD

- 4 Members and 1 Observer

- Appoints and Oversee Trustees

- IFRS FOUNDATION

- 22 TRUSTEES

- Appoint and Oversee board members and Raise Funds

The foundation flows into two components:

- IASB

- 16 Members (Maximum 3 part time)

- Sets Technical Agenda, Approve Standards, Exposure Drafts and Interpretations

- IFRS INTERPRETATIONs COMMITTEE

- 14 Members

- Work on Interpretations

What Constitutes Complete Set of IFRS?

IASC – International Accounting Standards Committee

- Publication of 41 IAS by IASC from 1973 to 2001 (not renamed)

IASB – International Accounting Standard Board

- Publication of 9 IFRS by IASB from 2001 to till date

SIC – Standing Interpretations Committee

- Publication of 32 interpretations by SIC from 1973 to 2001

IFRIC- International financial reporting interpretations committee

- Publication of 19 interpretations by IFRIC from 2001 to 2010

Note – In July 2010 interpretation committee name has been form International Financial Reporting Interpretation Committee (FRIC) to International Financial Reporting Standards Interpretation Committee (IFRS IC).

A Brief IFRS History:

1967 – AISG Accountants International Study group

1973 – IASC International accounting standards committee formed

1998 – Core Standards Completed

2000 – SEC review of core standards, IASC approves new constitution

2001 – EC proposes that all EU listed companies should apply IAS by 2005

2002 – EU decision to adopt IFRS from 1 Jan 2005 IASB and FASB signed Norwalk Agreement

2005 – Nearly 7000 listed companies switch to IFRS

2007 – ICAI issue concept paper on IFRS, SEC accepts filling from Foreign Privates Issues (FPI) without reconciliation to US GAAP

2008 – SEC issue Roadmap for transition to IFRS

2010 – IASC Foundation becomes IFRS Foundation

{kind=link}