Financial Accounting Vs. Managerial Accounting

A number of members of the Learning & Development group wanted to understand the distinction between Financial Accounting and Managerial Accounting.

Both these streams come from the base called ACCOUNTING. An entity decides to do a business, conducts its operations, financing and investing activities, offers a product or service to a marker or a community, records what it does and informs all connected with it in a reasonably summarized manner, what did it do and what it achieved.

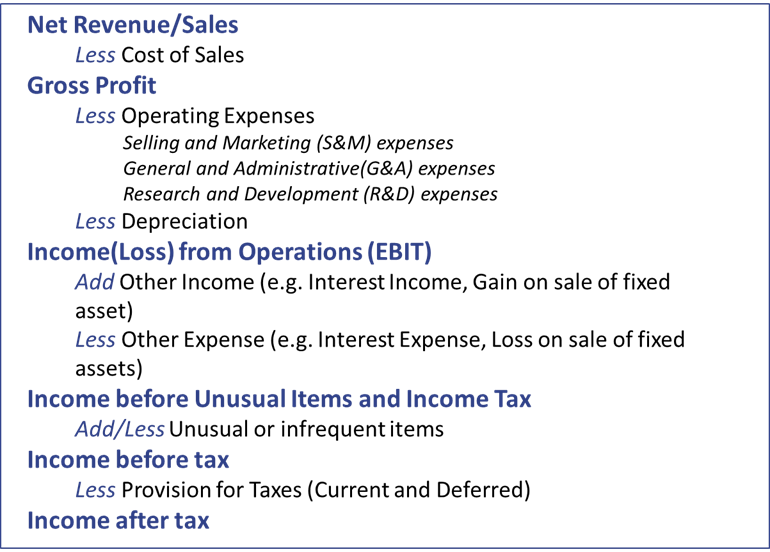

So, this business has an accounting department which accounted for all that it did, all that which could be measured in money terms. So, we can conclude that it did Financial Accounting.Thus financial accounting comprises of recording financial transactions, summarizing them for various stakeholders and reporting them, based on the law of the land and other practices in vogue n that region.

Over the years, the scope of Financial Accounting expanded and was separated in a logical manner from Accounting. Financial accounting has now evolved into a stream, providing information to stockholders, creditors, and others who are outside an organization. Financial accounting provides the scorecard by which a company’s past performance is judged. This information may be mandated by the laws in vogue, or by the business owners themselves, besides other business connects and stakeholders, including employees. It is majorly external in nature. Financial accounting is used to present the financial health of an organization to its external stakeholders. Board of directors, stockholders, financial institutions and other investors are the audience for financial accounting reports. Financial accounting presents a specific period of time in the past and enables the audience to see how the company has performed. Financial accounting reports must be filed on an annual basis, and for publically traded companies, the annual report must be made part of the public record.

Management or managerial accounting is primarily an internal activity. It attaches the need for management/a manager to accounting. It is used by managers to make decisions concerning the day-to-day operations of a business. It is based not on past performance, but on current and future trends, which does not allow for exact numbers. Because managers often have to make operation decisions in a short period of time in a fluctuating environment, management accounting relies heavily on forecasting of markets and trends.

Even if I look at a simple back office process of Order Processing, the project manager will derive conclusions from the volumes, transaction amounts etc., to plan his operations, inform the financial / buying trends to the senior management, this will be a basic form of management accounting.

In essence, Management accounting is a field of accounting that analyses and provides cost information to the internal management for the purposes of planning, controlling and decision making.

Management accounting refers to accounting information developed for managers within an organization. It is defined as “Management Accounting is the process of identification, measurement, accumulation, analysis, preparation, interpretation, and communication of information that used by management to plan, evaluate, and control within an entity and to assure appropriate use of an accountability for its resources” by CIMA. This is the phase of accounting concerned with providing information to managers for use in planning and controlling operations and in decision making.

Managerial accounting is concerned with providing information to managers i.e. people inside an organization who direct and control its operations.

As per Wikipedia – http://en.wikipedia.org/wiki/Comparison_of_management_accounting_and_financial_accounting

the differences between management accounting and financial accounting include:

- Management accounting provides information to people within an organization while financial accounting is mainly for those outside it, such as shareholders

- Financial accounting is required by law while management accounting is not. Specific standards and formats may be required for statutory accounts such as in the I.A.S (International Accounting Standard) within Europe.

- Financial accounting covers the entire organization while management accounting may be concerned with particular products or cost centres.

Managerial accounting is used primarily by those within a company or organization. Reports can be generated for any period of time such as daily, weekly or monthly. Reports are considered to be “future looking” and have forecasting value to those within the company.

Financial accounting is used primarily by those outside of a company or organization. Financial reports are usually created for a set period of time, such as a financial year or period. Financial reports are historically factual and have predictive value to those who wish to make financial decisions or investments in a company. Management Accounting is the branch of Accounting that deals primarily with confidential financial reports for the exclusive use of top management within an organization. These reports are prepared utilizing scientific and statistical methods to arrive at certain monetary values which are then used for decision making. Such reports may include:

- Sales Forecasting reports

- Budget analysis and comparative analysis

- Feasibility studies

- Merger and consolidation reports

Financial Accounting, on the other hand, concentrates on the production of financial reports, including the basic reporting requirements of profitability, liquidity, solvency and stability. Reports of this nature can be accessed by internal and external users such as the shareholders, the banks and the creditors.

Careers in these streams:

Both these streams do require an analytical bend of mind. An understanding of finance / accounting is almost mandatory, except in some limited situations. These streams are critical for decision making for almost all organizations. They form a part of the core support functions, and provide valuable inputs to the business, management and its stakeholder.

Every entity, whether into a business or executing a social / charitable responsibility needs different levels of financial / management accountants. In case of small activity entity, quite often it is the accountant who executes these functions.

For back office functions, like Record to Report(https://faoblog.com/category/finance-and-outsourcing/functions/record-to-report-functions/), teams are prepared for focused data collection and analysis.

For a job-seeker, some of these specialized activities can be learned through focused trainings. Over a period of time, as the individual job-seeker gains knowledge, practice and applies his analytical skills in a judicial manner, these activities translate into an elite job profile for the job-seeker / employee, which is valued and respected.

{kind=link}