Notification – IFRS

Dear Readers, We had a separate section on IFRS, however we have decided to close the same, since...

Read More

Dear Readers, We had a separate section on IFRS, however we have decided to close the same, since...

Read More

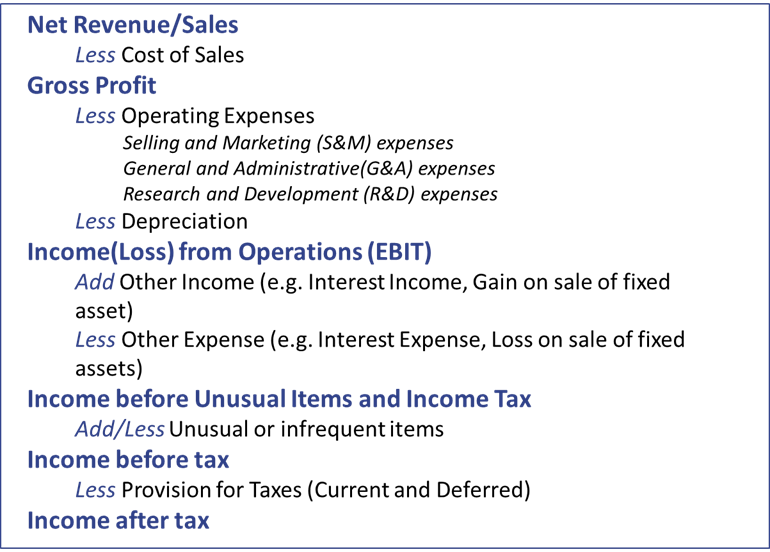

Final accounts – an understanding – Key statements In the last upload to the Learning &...

Read More

Effective Communication Happy Independence day to all our American readers. I have been itching to...

Read More

We introduced you to the three key statements of accounts in the Learning & Development...

Read More

Final accounts – an understanding – Key statements We introduced you to the three key statements...

Read More

Final accounts – an understanding – Key statements In the upload, as shared earlier in the...

Read More

Final accounts – an understanding – How it developed In the last upload, as shared in the...

Read More

I had earlier shared Part 1 of a case study on improving the recruitment process published by the...

Read More

Mid-size analyst upstarts are creating value faster. The analyst world is changing for the BPOs....

Read More

Final accounts – an understanding – The need In the last upload, as shared in the Learning &...

Read More

Successful Entrepreneurs Do These 5 Things Daily We saw this article on the Entrepreneur website....

Read More

Case Study: Improving Recruitment Processes iSixsigma network recently published a case study on...

Read More

Final accounts – an understanding – Importance of basic concepts In the last two uploads, as...

Read More

Why HR should be the strongest team in any organization We had shared an article on our blog...

Read More

Why HR should be the strongest team in any organization We had shared an article on our blog...

Read More

Why HR should be the strongest team in any organization We had shared an article on our blog...

Read More

Final accounts – an understanding In the previous post, as shared in the Learning &...

Read More

The iSixSigma Network recently shared a case study on a DMADV Approach to Marketing and...

Read More

Why HR should be the strongest team in any organization We had shared an article on our blog...

Read More

Why HR should be the strongest team in any organization We had shared an article on our blog...

Read More